What a difference a few weeks can make. Is the price of oil still relatively high? It sure is. But does the market care? Not from what I can see. While March finished with a pullback in the S&P 500 (SPY ETF) of around -8.88%, once April arrived, it rebounded into new all-time highs.

However, I should note that now, several weeks into this market rally, the strength of many sectors is starting to taper off. Technology (XLK ETF) has remained one of the stronger sectors. Sure, Energy had its day earlier this year, driven by the spike in oil prices related to the Iran conflict. The Energy (XLE ETF) is roughly the same price it was 52 trading days ago (FastTrack data).

The Federal Reserve got a new Chairman, Kevin Warsh, replacing Jerome Powell (who will remain a Fed governor). What we know so far is that his vision is to lower interest rates, shrink the Fed’s balance sheet, and believes AI and crypto will lead the way forward. Lower rates historically tend to support the stock market, so that could be positive if that can be achieved.

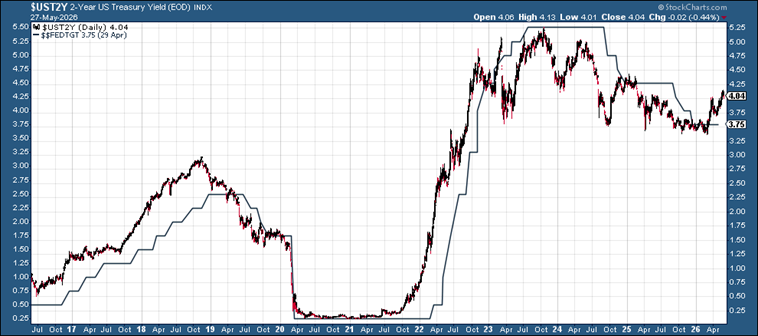

However, looking at the 2-year Treasury yield right now, some analysts have argued rates should probably be 0.25% higher than they are today. That agrees with Tom McClellan’s work that suggests the Fed Funds rate would be better off just following the 2-Year yield instead of a team of PhD’s. When you compare the two, he does make a good point.

In my May market update video, I spend some time at the end talking about UPI (Ulcer Performance Index) Scoring and how we are leaning into it more and more to help us evaluate investments through an additional risk-management lens. I’ve always been a fan of data and keeping an eye on factors that take into account and even prioritize drawdown when making comparisons. Is fund A better than fund B? That depends, but using this methodology can help us quantify the stress (thus the “Ulcer”) when the market goes through a rough patch.

This month’s chart is a look at the 2-year Treasury Yield vs. the Fed Funds rate (mentioned above). The yields shown have been sneaking upward over the past few weeks to just over 4.00% while the Fed Rate is at 3.75%. This is what we look at when trying to get an understanding of where the Federal Reserve is likely to be moving rates next. So while the new Fed governor wants to lower rates, this chart suggests the next change should be upwards to match the 2-year yield.

Ten-Year chart of the 2-Year Treasury Yield with the Fed Funds Rate (Source: StockCharts.com)

Our Shadowridge Long-Term Trend indicator has remained positive since April 8th, suggesting the market could continue moving higher. For now, we don’t see any signs of trouble in this data until it breaks below its trendline.

Our Mid-Term Cycle indicator turned positive on May 21st, after an interesting move lower in this data. All while the market continued to grind sideways and even slightly upwards. Even if the market isn’t going down when this indicator is falling, it does tend to suggest short-term headwinds to the market moving higher. But now that has resolved itself, and the positive momentum appears likely to continue.

As of Wednesday night (May 27th, 2026), our Shadowridge Dashboard showed Positive to Negative market sectors as 6 to 5. Technology has been the stand-out leader in the recent rally, while many other sectors have slowed down considerably. For now, the sectors that drive the market higher are still largely on the positive side. This is a 3rd positive metric suggesting positive health of the current market environment.

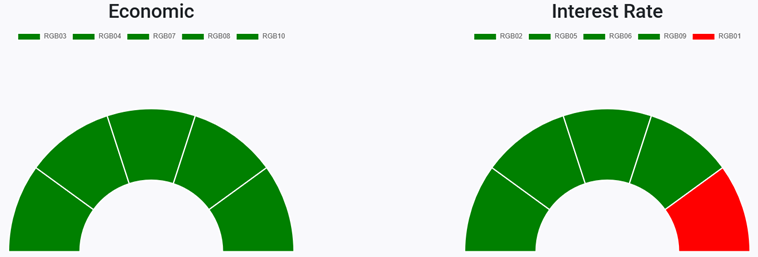

Right now, 9 RGB Bond Indexes are back to trending positive, all above their 50-day Moving Averages. Bond sectors have been messy this year, with many making frequent trips above and below their trendlines. For now, they look good, but as we’ve said many times in the past, we continue to question whether core bond sectors will provide the same diversification benefits they historically have.

RGB Economic and Interest Rate Sensitive Bond sectors (Source: ShadowridgeData.com)

Traditional Bond sectors continue to offer limited diversification benefits during periods of volatility. The 7-10 year Treasuries (IEF) and the Aggregate Bond Index (AGG) are both close to flat on the year so far. We still find limited benefit in these traditional asset classes. Bond holdings are often the first area we can improve when we are asked to review portfolios managed elsewhere. Too many traditional allocators are still using parts of this asset class that may offer little benefit to overall portfolio resilience in times of market stress.

Bottom Line: Awesome rebound in the market off of the Q1 pullback, but the leadership is shrinking to mostly the Technology sector. The bond market isn’t offering much value in diversification, so we continue to remain selective in those areas. However, several other asset classes like Bank Loans, Arbitrage, and Market Neutral funds have helped us reduce portfolio drawdowns and helped to keep client “ulcers” to a minimum.

Stay safe out there!

Shadowridge Asset Management, LLC is a registered investment adviser. Advisory services are only offered to clients or prospective clients where Shadowridge and its representatives are properly licensed or exempt from licensure. This content is for informational purposes only and should not be construed as personalized investment, tax, or legal advice. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results.

1 The Standard and Poor’s 500 is an unmanaged, capitalization-weighted benchmark that tracks broad-based changes in the U.S. stock market. This index of 500 common stocks is comprised of 400 industrial, 20 transportation, 40 utility, and 40 financial companies representing major U.S. industry sectors. The index is calculated on a total return basis with dividends reinvested and is not available for direct investment.

2 Charts are for informational purposes only and are not intended to be a projection or prediction of current or future performance of any specific product. All financial products have an element of risk and may experience loss. Past performance is not indicative of future results.